This column doesn’t offer investment advice, as I am not a registered investment advisor. This is not merely a mandatory disclaimer; this is a warning. We will discuss some specific securities below that I am not merely incapable of recommending.

Finance performs a strange alchemy, teleporting value through time and space. Ordinarily, Bits about Money focuses more on the plumbing of it than the deals. But a deal enthusiast who goes by The Conservative Income Investor recently flagged a capital raise to me. It has everything: echoes of the culture that is the American PMC 2020-2024, complex financial structuring, a novel web application to move money, a crypto company in the background, and municipal politics. So it seems squarely within this column’s beat.

The municipality happens to be Chicago, my hometown and (after a 20 year stint in Japan) current residence. And so I feel some sense of civic duty, as a Chicagoan, taxpayer, and reasonably financially sophisticated person, to say the following publicly: What the hell, Chicago.

But before we get to present-day shenanigans, we need to go back several decades, because municipal politics is inextricable from the shenanigans.

Chicago has wanted a casino for a long time

Chicago and the state of Illinois more broadly have a deeply unserious polity. It has mortgaged its future through consistently overpaying public sector employees (principally, in Chicago, police/fire/teachers) and undertaxing. Neither decreasing total compensation of public sector employees nor reneging on previously-negotiated deferred compensation (pensions and healthcare for retirees) nor raising taxes to appropriate levels is considered politically palatable. One reason is that the Illinois state constitution (Article 13 Section 5) makes public employee pensions sacrosanct. The constitution is, of course, not a fact of nature; it is a political compromise by, again, a deeply unserious polity.

Long-time watchers of state and local politics know Illinois pensions are the worst funded in the nation, state officials celebrate when Wall Street upgrades its credit rating from close-to-junk, and the possibility of a federal bailout was a constant political issue for decades until it happened by stealth during covid.

And so Illinois and Chicago specifically are constantly on the make for new revenue streams. One which was mooted since my childhood in the 1980s was an expansion of gambling. So-called sin taxes (on gambling, liquor, tobacco, and similar) are politically attractive because they do not cause as much opposition as raising consumption or property taxes.

And so Chicago has had a decades-long campaign to build a casino within city limits. Why couldn’t Chicago actually get this done in several decades? One reason is the usual incompetence. The other reason is that the political economy of casinos is controversial. Many policies create winners and losers, but casinos inescapably create losers much more directly than most policies up for vote. Local political elites often band together against them, worried about siphoning money from local consumers. They also worry that they tend to create spillover effects, such as crime and moral collapse among a portion of patrons.

And so, as I once mentioned in a podcast with Thinking Poker, pro-casino political coalitions try to pick off anti-casino political elites by assuaging their concerns and/or bribing them. (In Japan, the de facto concession was “We’ll limit the amount Japanese people can lose here and maximize for soaking Chinese tourists. Now, let’s write that down in a way which doesn’t say exactly that, because it sounds bad if you put it that way.”)

In Chicago, much of the opposition came from African American political elites. They had the usual set of concerns for casinos, plus one other which is slightly more idiosyncratic. A belief with wide currency in that community is that the community would be much more wealthy than it currently is, but for vice entrepreneurs siphoning that community’s resources out of the community. This belief has lead to e.g. pogroms against Korean liquor store owners. I direct interested readers to histories of the Rodney King riots or the Asian American experience in 20th century America. (This was covered extensively in an elective I took more than 20 years ago, and so I have since forgotten the academic citations for this true but parenthetical point.)

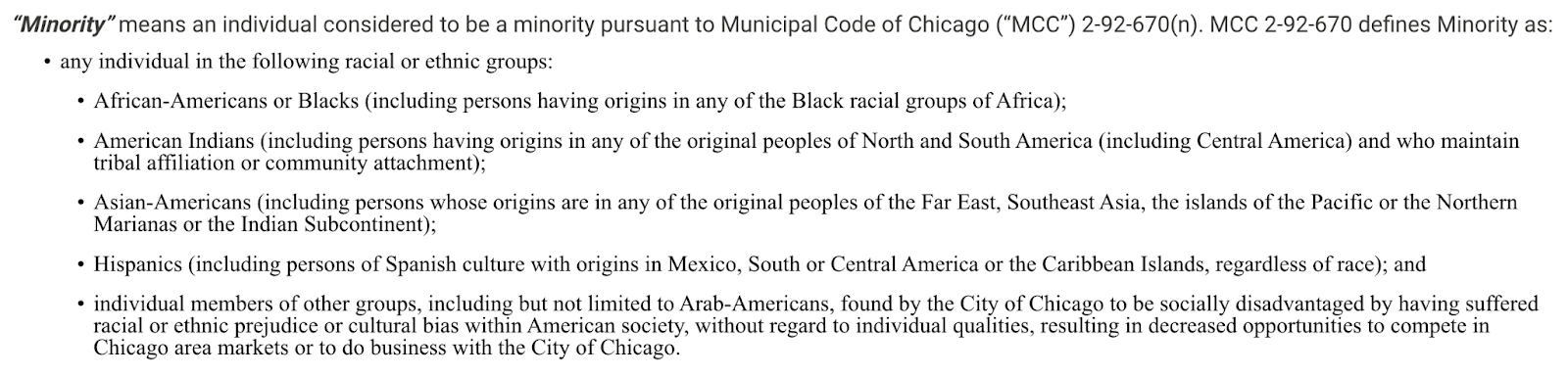

Bally’s won the bid for the newly licensed Chicago casino in 2022, in part due to offering the right mix of concessions and inducements in its Host Community Agreement. One of those was promising Chicago that the new casino would be at least 25% owned by women and Minorities. The M is capital in the Chicago municipal code, and I will preserve this stylistic choice, because the word does not mean what most educated Americans assume it means. We shall return to that meaning later.

The stock offering

In fulfillment of its obligations under the HCA, Bally’s Chicago, Inc., an entity in the corporate web which will build and operate the casino, has conducted a stock offering since December. It runs through January 2025.

The stock offering has a prospectus associated with it. BCI does not appear to be relying on an exemption from registration, in the fashion that e.g. most startups would, restricting them to raising money from accredited investors.

While reading the prospectus, I read a much-remarked-upon statement, and assumed it was a misprint.

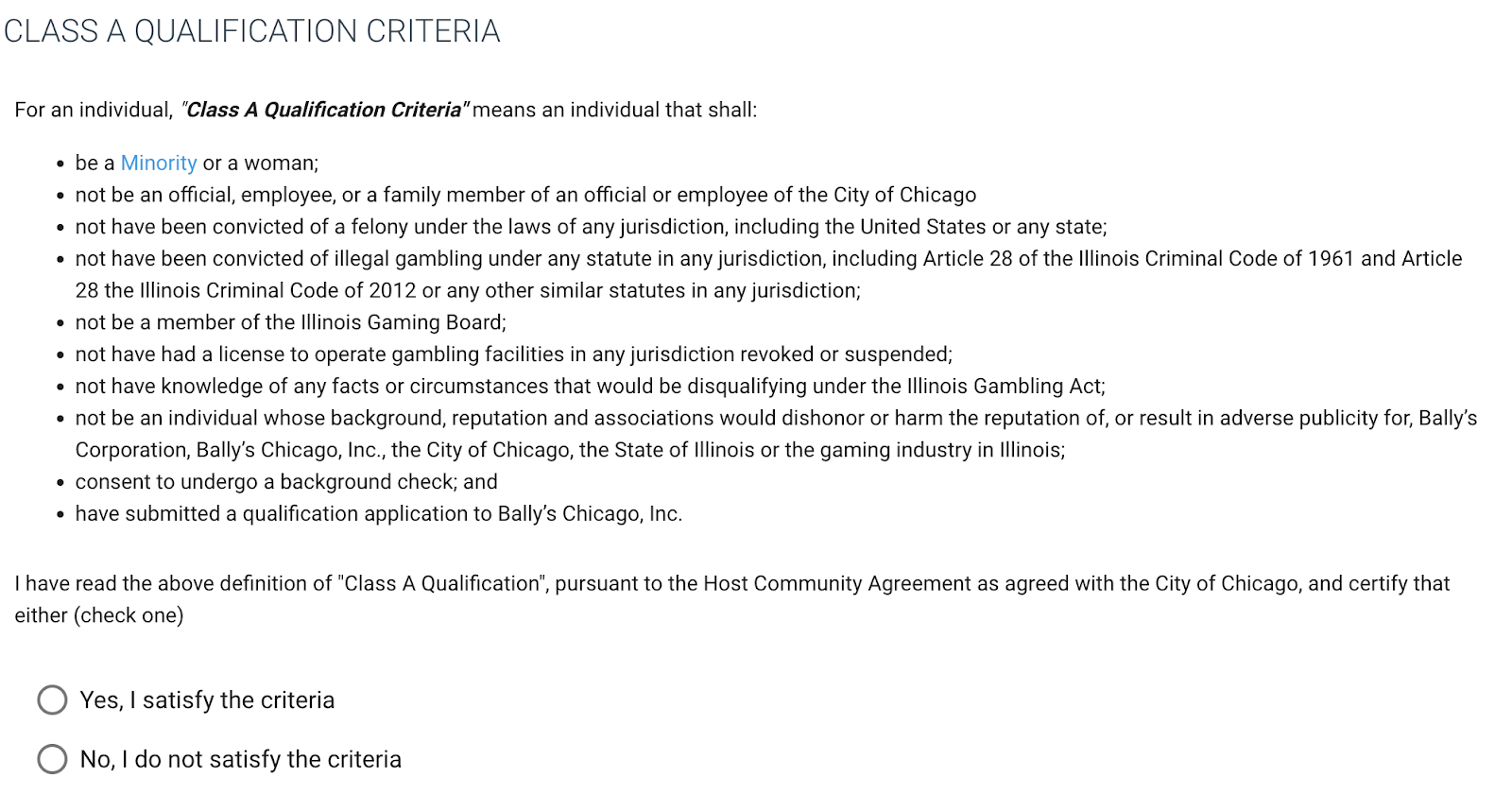

This offering is only being made to individuals and entities that satisfy the Class A Qualification Criteria (as defined herein). Our Host Community Agreement with the City of Chicago requires that 25% of Bally’s Chicago OpCo’s equity must be owned by persons that have satisfied the Class A Qualification Criteria. The Class A Qualification Criteria include, among other criteria, that the person:

- if an individual, must be a woman;

- if an individual, must be a Minority, as defined by MCC 2-92-670(n) (see below); or

- if an entity, must be controlled by women or Minorities.

Why did I assume this was a mistake? Well, for one thing, on the face of it Bally’s has told the SEC that this offering is only available to Minorities who are also women, which does not match the intent expressed elsewhere or during their roadshow. I have immense sympathy for drafting errors. Bally’s, feel free to let the lawyers know they forgot a significant “or” on the first bullet point. [Post-publication edit: An actual lawyer, not an Internet lawyer, informs me that the first bullet point has an implied "or" in this construction. Mea maxima culpa, associate who drafted this.]

The other reason I thought this was likely a mistake is that the American social, legal, and constitutional order is profoundly opposed to discrimination by race, and considers that action malum in se. Even when individual actors want to do it, they usually feel embarrassed enough about it to dissemble.

For example, the last few years tech companies absolutely, notoriously engaged in legally prohibited discrimination in hiring, sometimes as an intentionally directed and explicitly written down policy. This is often assumed to be a conspiracy theory by disaffected white males. Perhaps that is an understandable belief, since people who read the project plans either a) supported them or b) value their future careers and are therefore mostly not leaking them, and thus we only have public evidence of those project plans which end up screenshotted in litigation. Similarly, when I say that the state of California proudly engaged in redlining in the provision of lifesaving medical care in 2021, many people of good-will assume that I simply must be mistaken. I get it, but I was there.

Returning from the ancient history of 2021 to this very week: Chicago has directed a private entity to segregate, and that entity is segregating, principally via web application. If you attempt to engage Bally’s for an investment here, you will see the following blocking question during qualification stages for the investment opportunity. (The web application will also ask for your name, address, social security number, and accredited investor status.)

There is a right answer to this question. If you give the wrong answer, Bally’s will decline you the opportunity to invest. You get entirely stopped by the web application.

I express no opinion on whether this is legal, by Bally’s or Chicago. After all, I am not a lawyer, and this has certainly been seen by many lawyers at this point, in e.g. preparing the submission to the SEC. Presumably all of them went through 1L courses which introduced concepts like the Fourteenth Amendment, case law which says government actions discriminating by race are subject to strict scrutiny, and case law which says that the government cannot proxy through a private entity to do things it is prohibited to do itself. And clearly no one admitted to the bar in Illinois thinks that Chicago can waive the U.S. Constitution if it considers that politically advantageous to get a gridlocked casino through municipal politics.

So I will charitably assume the existence of a memo where competent professionals have laid out a case for the legality of this course of action. They must have concluded that no future Department of Justice Civil Rights Division, not even in an administration elected after the Host Community Agreement had been inked, would descend upon this official act like the hammer of an avenging god.

As Matt Levine beat me to observing: awkward timing.

Chicago’s peculiar definition of Minority

Long-time observers of Chicago politics might opine that the city very rarely does anything without creating a carveout for politically connected individuals. The local phrase for this sort of social connection is having “clout” or, sometimes, “is clouted.” You can find examples of the sort of carveouts Chicago reserves for the clouted in the professional histories of the board members of Bally’s Chicago, Inc, for example, which are included in the prospectus.

So what’s the carveout here? The definition of a racial or ethnic minority is a legendarily contentious one in U.S. politics, largely because inclusion or exclusion from it makes one eligible (or ineligible) for concrete benefits. Sites of contention often include e.g. are Asian Americans a minority, or are e.g. Cuban Americans Hispanic, etc.

Chicago leaves itself an out for its definition of Minority, which lets it designate any individual or group as a Minority, on an ad hoc, unreported, unaccountable basis. That sounds like I must be strawmanning Chicago. See the below screenshot and explanation in the prospectus

Quoting the prospectus:

Qualification under [the final] clause is determined on a case-by-case basis and there is no exhaustive or definitive list of groups or individuals that the City of Chicago has determined to qualify as Minority under this clause. However, in the event the City of Chicago identifies any additional groups or individuals as falling under this clause in the future, members of such groups would satisfy the Class A Qualification Criteria.

Now, fairminded people reading “groups… found by the City of Chicago to be socially disadvantaged by having suffered racial or ethnic prejudice or cultural bias within American society” would note “Well, OK, on the face of it, that definitely includes e.g. Jewish Americans or Irish Americans. We have some lamentable history as a nation and city, sure. But no intellectually serious person in the United States considers Irish Americans ‘a racial or ethnic minority’ in the common usage of the term.” And thus, the capitalization of Minority.

You’ll have to ask the city for their list of ad hoc exceptions made under this bullet point. Long-time watchers of Chicago municipal politics, however, might say that asking is of limited utility.

I will note that, as a matter of engineering fact, the web application will blithely accept self-certification under this bullet point for anyone. You are welcome to your guess as to whether Bally’s or any city employee will review the 1,000 investors individually and, if they review them, what the process is for determining whether e.g. a particular Patrick counts as a Minority or not.

I’d wager there is no process at all here. It seems like a better bet than most offered in the casino.

Reading a complex corporate structure

Bally’s Chicago is a product of Bally’s, a publicly traded company. You can read their 10-Ks. According to their most recent quarterly report, they operate 15 casinos across the U.S., and have substantial online gambling operations. Like many casinos, they are somewhat diversified, insofar as a casino resort also functions as a hotel and restaurant/bar/etc venue.

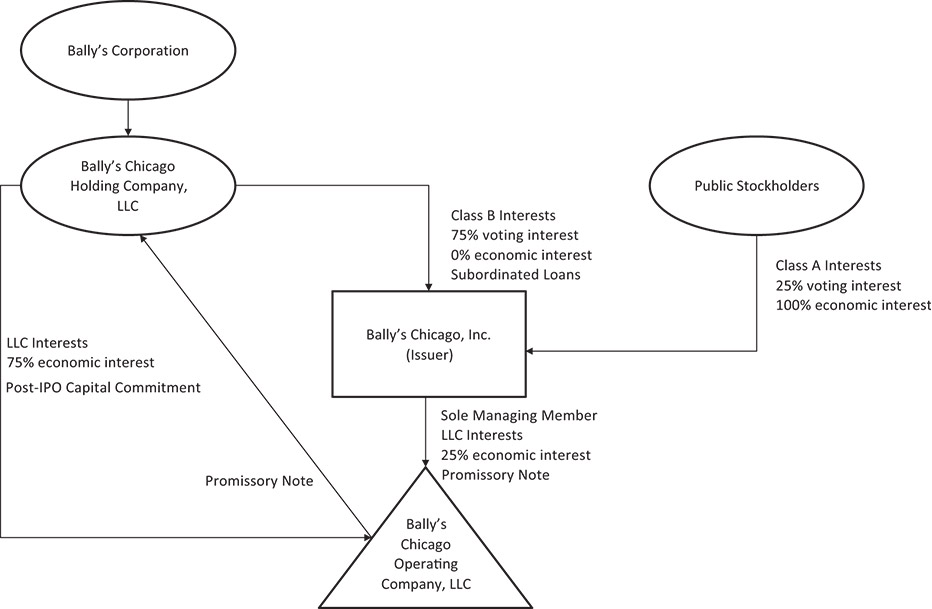

Bally’s Chicago has a complex capital stack, which one would probably need to understand to evaluate the opportunity to invest in it. I am not saying “complex” as a criticism: this is fairly ho hum by the standards of large commercial real estate developments, a subject I am not an expert on but grew up hearing about at the dinner table. I am heavily implying that I would not expect a Chicagoan picked at random, or for that matter an alderman, to be able to look at the following diagram and correctly describe what it means. Prospectus, ibid, pg 145.

The entity which Chicago is stumping for is Bally’s Chicago, Inc. (BCI), the central square on that diagram. Marks investors are receiving ownership in that entity, not in the casino, which will be operated by Bally’s Chicago Operating Company, LLC (BCOC). That entity gets 25% economic interest in the future profits (insert very material asterisk here) of the casino; the other 75% flows to Bally’s Chicago Holding Company, LLC (BCHC). BCHC is a wholly-owned subsidiary of Bally’s, Inc, the publicly traded company.

When one offers someone the opportunity to invest in something, one has to decide upon a valuation for the something. The price of a slice of the pie is set in notional reference to the price of the whole pie.

Bally’s says that its good faith guesstimate on the whole pie is the economic interest in future profits of the Chicago casino is… a billion dollars exactly. The prospectus, as is wont for these situations, disclaims floridly that that price might not be accurate. One example of many: “We made a number of assumptions to determine the price of our Class A Interests. If any of our assumptions are incorrect, including our assumptions regarding the total enterprise value of the Company, then the Class A Interests will be worth less than the price stated in this prospectus. In such case, the return on investment or rate of return on an investment in our Class A Interests could be significantly below an investor’s expectation.”

Bally’s will, as is standard and customary for this sort of thing, pretend that investors have read and understood the ~200 page prospectus, and civil society will pretend to believe them.

It isn’t extremely improper to pick a billion dollars out of one’s hindquarters as an investment valuation. That particular number exerts a sort of memetic quality in e.g. Silicon Valley, and there are legendary amounts of negotiation between sophisticated parties to accept just a bit more structure to get a e.g. $920 million valuation to a $1 billion valuation, because so-called unicorn status is good for PR, for attracting prospective employees, and (a real factor) for founder ego.

But if you invest at a valuation not justified by the fundamentals of the investment, you will tend to underperform. This is an inescapable fact of investing. (And that is why the sophisticated investors, accepting a “worse” valuation, want “better” structure to compensate for it.)

And this partially explains why Chicago is holding a roadshow in African American churches attempting to convince participants to invest in a mezzanine-y equity slice of a casino at a $1 billion valuation, perhaps at 100X leverage. (I tip my cap to publicly available reporting of the roadshow.) And not, for example, attempting to convince Goldman Sachs to put together some sophisticated investors and take down the $250 million allocation.

Is this valuation a gift to investors?

Chicago’s pitch to investors, delivered (per above reporting by Triibe) by “City Treasurer Melissa Conyears-Ervin and members of the Chicago Aldermanic Black Caucus”, emphasizes the potential of creating “generational wealth” (direct quote) with this casino investment. This point of view aligns with the above described political economy of attempting to buy off influential communities and/or community elites with an equity carveout, which successfully got this particular casino through decades of political gridlock.

And so the investment case implies that Bally’s is intentionally giving takers something for nothing. That is, they must be sandbagging the valuation they assigned to this bundle of rights: it’s not really worth $1 billion, it is worth e.g. $5 billion. Only you favored Chicagoans well-loved by your alderman are able to buy at the non-market price, leading to essentially free money. Not merely small amounts of it, either. Generational. Wealth.

The pitch very likely explicitly said the requisite words about this being a risky investment, wink wink, and very definitely described an opportunity for extreme levels of leverage and a lengthy expected road to ROI, which we’ll return to in a moment.

Do I think sophisticated investors would agree with Bally’s that this bundle of rights is worth $1 billion? Reader, I do not.

One reason is the perception of an absence: why is this pitch being given to individual savers in a church at a minimum investment of $250, and not in a swank office to an entity capable of committing $25 million? But perhaps I’m just suspicious.

No, let’s go to more direct evidence: if 25% of this bundle of rights is worth $250 million, then 75% must be worth $750 million, right? And if an entity owning 75% of the bundle, Bally’s, also owns 14 other casinos, online gambling properties, and similar, then that entity must be worth a lot more than $750 million, right?

The market does not agree with this assessment. The entire market capitalization of Bally’s (NYSE: BALY) is, as of this writing, ~$1.5 billion. What’s the difference between the $50 million average imputed value of the other casinos and the $750 million imputed value of the Chicago casino? The $750 million is made up, that’s what.

And, again, the real unspoken logic of this pitch is that the bundle of rights is getting sold on the cheap, and that it is actually worth much more than $1 billion. It very clearly is not, or sophisticated investors would be swooping in and buying BALY’s common stock. Crack it open like an oyster and dig into that sweet sweet Chicago gambling revenue if you need to!

This is somewhat elementary and handwavy napkin analysis of a complicated business which, like most casinos and hotels, is heavily levered with a complex capital stack. But the investment case gets smothered by a napkin.

Capital stack arbitrage, or, giving retail 100:1 leverage on single stock issuances

The Host Community Agreement, as above, obligates Bally’s to find a way to sell preferred Chicagoans $250 million of stock. This was likely complicated by rich Chicagoans not being suckers and less-well-off Chicagoans not having $250 million lying around.

And so Bally’s has introduced a novel structure.

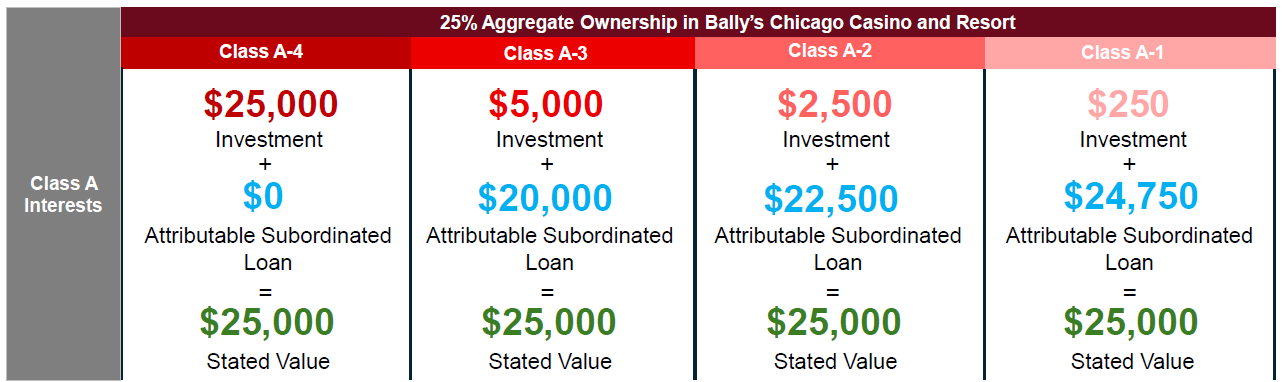

In brief, that structure sells stock to investors on credit, with the credit being extended by Bally’s, and paid down by future dividend distributions of the stock. If you’re very interested in the mechanics, you can find them at length in the prospectus, but the complex legal code is an excuse for this screenshot:

What is the “Attributable Subordinated Loan?” I’m glad you asked. Bally’s staked (ba dum bum) BCI with a few hundred million dollars to fund development. Where did it find the money to do that? A mix of equity and debt financing, as is common for virtually all complex commercial real estate transactions. Bally’s, per their most recent 10-K, has long-term debt from sophisticated investors which costs them 5.x% per year. (It would be more expensive if they wanted to lock that down today.)

In return for Bally’s advancing BCI money through BCHC, BCI owed BCHC money, on an intercompany IOU. This capital offering cancels that intercompany IOU and replaces it with the Subordinated Loans. The prospectus does not quote the rate that the left pocket of Bally’s charged the right pocket of Bally’s. It does quote the rate for the Subordinated Loans: 11% annually compounding quarterly.

The road show makes much of the fact that this leverage is non-recourse. Quoting the Triibe reporting again:

The loan is non-recourse, explained Sidney Dillard of Loop Capital Markets, who is the underwriter of the offering, during the information session. “That loan is not recourse, meaning that you are not responsible for it,” she said.

I am not someone who has ever offered SEC-registered securities for sale, but I am aware that when one does that, one has to adopt a certain level of care with respect to how one simultaneously a) sells a product that one has to offer and b) describes the operations of that product without wandering into lying.

And so this writer would not describe “non-recourse” as a loan one is not responsible for. I have a non-recourse mortgage. I am very, very much responsible for paying the mortgage. If I do not pay the mortgage, I expect to swiftly not own the property securing the mortgage. The “non-recourse” bit means that the lender cannot come after your other assets or income, for example by suing you for a judgement, then forcing you to disgorge your savings account or e.g. interests you own in your small business' LLC.

The Subordinated Loans are, per the prospectus (probably a bit more reliable than the understanding of e.g. Chicago employees on the finer details), not between the owners of the Class A-{1,2,3} equity and any Bally’s entities. They are strictly loans between Bally’s entities themselves. Those loans are senior to Class A-{1,2,3} equity in the payments waterfall of future profits (we need that asterisk again!) from the casino to equity holders. The expectation is that Bally’s will individually book repayments against records which are kept on a per-shareholder basis without actually obligating the shareholder, while keeping the actual cash thrown off by the casino, prior to eventually releasing a shareholder from the indebtedness that Bally’s will say that, technically speaking, they have not actually incurred.

At that point, the shareholder will own the slice of equity that an unsophisticated listener of that roadshow might think they own free-and-clear.

Now, Bally’s forecasts that many shareholders will be very underwater on these investments. (Wow, that’s a robust sentence.) Prospectus, ibid, pg 23:

Given the capital intensity of developing, constructing, opening and operating a casino resort project of this scale, we currently expect that Bally’s Chicago OpCo will not have any OpCo cash available for distribution until approximately three to five years after our permanent resort and casino begins operations.

Assuming the most charitable estimate from that range, a Class A-1 shareholder will have $250 of equity securing a notional $25,000 investment and future obligations of approximately $34,000 (three years of compound interest at 11% on initial principal of $24,750). This suggests that the holder’s equity value is planned to be negative and that no sophisticated investor would purchase that investment for the $25,000 which the unsophisticated shareholder might believe it to be worth in 3 years. They might be willing to pay something more similar to, hmm, negative nine thousand dollars.

Seen in that light this offer of investment sounds predatory. But don’t worry, Chicagoans, Bally’s has your back. You do not have to worry about not being able to sell your stock due to its lack of intrinsic value, because you are not able to sell your stock. Prospectus, ibid, pg 179 under heading Shares Eligible For Future Sale, and elsewhere in the document.

Class A-4 holders, the ones with no notional debt, who purchased their shares for $25,000 cash-on-the-barrel, are not eligible to sell their stock at any time except as allowed by Bally’s to people approved by Bally’s. (I’ll flag that this is not an unusual term in private equities. Bally’s pre-commitment to discriminating racially against future prospective buyers? That’s unusual.)

Buyers of Class A-{1,2,3} stock are unable to sell until the associated Subordinated Loan is paid off in full.

One wonders whether senior Chicago officials will be doing a roadshow in 2030 explaining what happened.

The casino will not distribute profits, per se

While the natural expectation is that one is participating in the profits of the casino, the prospectus helpfully clarifies that one is not. The "cash available for distribution" does not necessarily correspond 1:1 with profits. It... well. See the discussion on page 22 and 23 of the prospectus, including the excerpt below.

While we and Bally’s Chicago OpCo intend to make distributions equal to 100% of the cash available for distribution and OpCo cash available for distribution, respectively, on a quarterly basis, the actual amount of any distributions may fluctuate depending on our and Bally’s Chicago OpCo’s ability to generate cash from operations and our and Bally’s Chicago OpCo’s cash flow needs, which, among other things, may be impacted by debt service payments on our or Bally’s Chicago OpCo’s senior indebtedness, capital expenditures, potential expansion opportunities and the availability of financing alternatives, the need to service any future indebtedness or other liquidity needs and general industry and business conditions, including the pace of the construction and development of our permanent resort and casino in Chicago. Our Board will have full discretion on how to deploy cash available for distribution, including the payment of dividends. Any debt we or Bally’s Chicago OpCo may incur in the future is likely to restrict our and Bally’s Chicago OpCo ability to pay dividends or distributions, and such restriction may prohibit us and Bally’s Chicago OpCo from making distributions, or reduce the amount of cash available for distribution and OpCo cash available for distribution.

Now, as someone who grew up with a father constantly complaining about sharp operating in Chicago commercial real estate, I can quickly outline about two dozen different ways for one to cause the operating company here to a) transfer money to other corporate entities and b) therefore have less cash available for distribution.

As a representative but not limiting example, you can probably choose your own marks for technology services from a parent to a great-grandchild subsidiary. Sure, there is some notional expectation that the marks be at arms-length price, but what is the arms-length price for e.g. casino loyalty accounting software and a particular chain's database of existing users? What low-resourced investor could possibly mount a court challenge against the entity with all the data necessary to value that asset. In Las Vegas, a casino has to calculate and diligently communicate the house edge before raking punters. Here... not so much.

That would require sharp operating... of a sort which is extremely routine in Chicago commercial real estate. This is a constant risk of being the junior partner in a structure, particularly without an aligned senior partner who would be as adversely impacted by sharp operating as you would be. Of course, here the senior partner owns e.g. the database they are renting to the entity that they also control, and so funds available for distribution from that entity might not match the expectations of junior partners.

Pick your sponsors carefully, folks.

Tax consequences of this offering

Suppose, and this is very unlikely because it is illegal (Reg T) but run with it, that one has a typical brokerage account in the United States and, with $250, purchases $25,000 of marketable securities. Those securities periodically throw off dividend payments. One periodically pays one’s brokerage interest, because one has borrowed money from the brokerage to buy those securities on margin.

In the typical case, one would be taxed upon those interest payments, which are income. One does not simply net one’s margin interest against that income before paying taxes. One instead must itemize deductions, and then one will be able to (on Schedule A) deduct investment expenses, as described in Publication 550. Feel free to run this by your accountant; the details get complicated and wonky.

If one does not itemize, as many lower-income taxpayers do not, one must of course simply pay the tax on the entirety of one’s interest income. If one protests that one does not actually have any interest income, because it has been taken by one’s brokerage to pay margin interest, the IRS will not be maximally sympathetic.

Bally’s has very creative professionals involved in the structuring of this offering, and realizing the above issue would compromise fitness for purpose, they have… adopted a theory. I will quote that theory, from the prospectus, verbatim. I have taken the liberty of bolding an important bit in the middle of this.

Section 305 of the Internal Revenue Code provides that if a corporation distributes property to some shareholders and other shareholders have an increase in their proportionate interests in the assets or earnings and profits of the corporation, such other shareholders may be deemed to receive a distribution that could be a taxable dividend. In this case, because we and Bally’s expect to treat the Subordinated Loans as “stock” for U.S. federal income tax purposes, “property” distributions will likely be considered to be made to “some shareholders” of Bally’s Chicago, Inc. as payments are made on the Subordinated Loans, and equivalent cash (“property”) distributions will be made with respect to the Class A-4 Interests. In addition, as payments are made on the Subordinated Loans, particularly those that repay the original principal amount of such Subordinated Loans, the proportionate interests of holders of our Class A-1 Interests, Class A-2 Interests and Class A-3 Interests in the assets or earnings and profits of Bally’s Chicago, Inc. may be viewed as increasing. Accordingly, it is possible that such increase could be treated as a deemed distribution under Section 305 of the Code or otherwise as taxable income to such holders under other theories. However, under the Treasury Regulations relating to Section 305 of the Code and other IRS administrative guidance, certain financing arrangements in the form of preferred stock investments that fund a corporation and then are systematically eliminated through property distributions until they are fully retired, and are designed to facilitate the ownership of a business with an effect of increasing another stockholder’s proportionate interests in the assets or earnings and profits of a corporation over such period, do not result in a deemed distribution to such other stockholder. The applicability of these authorities to the holders of our Class A-1 Interests, Class A-2 Interests and Class A-3 Interests in this situation is uncertain. Although the matter is not free from doubt, we intend to take the position, and this discussion assumes, that U.S. Holders of applicable series of Class A Interests would not be treated as receiving a deemed distribution from us or otherwise realizing income as a result of repayment of the Subordinated Loans corresponding to such shares. However, there can be no assurance that the IRS will not take a contrary position, for example, treating the proportionate interest in our earnings and profits owned by U.S. Holders of the applicable series of Class A Interests as having increased upon repayment of the Subordinated Loans corresponding to such shares, and treating such U.S. Holders as having received a distribution. In that case, such deemed distribution will be taxable as a dividend, return of capital or capital gain as described above under “— Distributions,” and U.S. Holders may be subject to U.S. federal income tax without the receipt of any cash. U.S. Holders should consult their own tax advisors about the application of Code Section 305 and any other potential deemed receipt of income risk with respect to our Class A Interests .

Now, I’m neither a lawyer, tax accountant, nor am I someone who listened carefully to the roadshow when it doubtlessly stepped through this for the benefit of the audience. But here’s what it means:

Bally’s is taking the position, though they acknowledge that the IRS might disagree, that owners of the Class A-{2,3,4} interests aren’t actually getting any income until the Subordinated Loans have been paid in full. This means that they don’t have to pay income taxes in years where they are not actually receiving cash distributions.

No, they wait until the Subordinated Loan is paid in full, and then immediately owe income taxes in one whack, at the difference between their basis in the stock (say, $250) and the then-FMV of the stock (say, $25,000). Resulting in Bally’s diligently filing a document with the IRS saying that e.g. a lower-income Chicagoan has just received a bit less than $25,000 in income from them, and should probably pay taxes on it. You can, of course, receive income without receiving immediately available cash; it happens all the time in tech, and is the cause of much structuring to avoid the consequences of it, which can be painful for e.g. early career employees.

Those taxes will be paid substantially out-of-pocket, because there is almost no conceivable universe where a stock of an actual healthy operating enterprise worth e.g. $25,000 pays an ordinary dividend of e.g. $5,000. The market would adjust the value of the stock upwards to account for the extraordinarily rich stream of dividends, which would adjust the tax bill upwards.

Financially sophisticated investors might prepare for a tax bomb like this by e.g. borrowing against the value of the stock. That’s basically impossible for this issuance, due to the stock not being publicly listed, the restrictions on transfer, small dollar amounts, etc. The other option is, of course, selling the stock, to whomever Bally’s deigns to approve.

Tax-motivated transactions are, of course, motivated transactions, and the lucky buyer will probably be able to extract a bit of a deal, doubly so because they are likely much more sophisticated than the initial buyer of the stock, and they have less risk to account for (because of e.g. several years of operating history of the casino before the tax bomb explodes).

In conclusion

I am not an investment advisor, and not your investment advisor. I am, however, a recreational poker player who lives in Chicago. I intend to periodically donate money to the Chicago economy by making poor decisions on the river at Bally’s Chicago.

I do not, however, presently intend to participate in Bally’s stock offering, nor do I presently intend to buy their common stock.

I will note, out of an overabundance of scrupulousness, that I own a tiny amount of MGM stock, which is a direct competitor to Bally’s. I caught the poker bug at a conference in Las Vegas (hosted at the Tropicana, since acquired by Bally’s and then brought down in a controlled implosion).

MGM, across the street, actually had poker tables. I have had many enjoyable post-conference excursions staying at their hotel to (in several but not all years) lose money at those tables. I bought the stock for the same reason I buy stock in every hotel, airline, bank, and similar I use: in the unlikely event a not-particularly-high-stakes poker player has a routine customer service complaint, Investor Relations is available as an escalation strategy, over e.g. hotel staff who might be long-since inured to listening to complaints from people who lost money in a casino.

Oh yeah, I mentioned that there is a crypto angle to this. The registrar and transfer agent for offering 100:1 leverage to retail investors on a casino stock is, see prospectus pg 41, BitGo Trust. If I had made up that detail, as a crypto skeptic, you might have accused me of being a bit on the nose.

Want more essays in your inbox?

I write about the intersection of tech and finance, approximately biweekly. It's free.