In the sciences they call it the file drawer problem: studies that fail to achieve significance or reach the "wrong" conclusion end up hidden away, creating a distorted picture of reality.

And so here's me rescuing something from the file drawer of banking procedure: a tale of two Americas, one bank branch, and $50,000 in cash.

A style magazine published an account of a large cash withdrawal that didn't match my understanding of banking reality. I burned several thousand dollars and a year investigating. I now doubt that account less, because I understand the context better.

Suppose you ask a bank to withdraw $50,000 in cash

There exist thousands of banks in the United States, each one independently operated with their own procedures, work forces, and circumstances. They are, broadly, similarly constrained by regulation, industry practice, culture, and perception of the threat environment. There is no such thing as a perfectly typical bank, banker, or banking client. But if we were to ignore the messiness of the real world, for the purpose of making a larger point, here is what is supposed to happen when a customer comes in and asks to withdraw $50,000.

A bank doesn’t expect its CEO or Head of Compliance to individually make decisions on every withdrawal. It has designed procedures to achieve the outcomes it (and its regulators, and other stakeholders) desire, and trained staff in how to implement those procedures. Those procedures happen to very explicitly contemplate this transaction.

The teller or personal banker, junior though they may be, is supposed to ascertain the identity of the customer, and ask themselves whether this is a typical transaction for this customer. Do they, perhaps, run a cash-heavy business which, every few weeks, takes out $50,000 to e.g. stock the ATM fleet they operate? If yes, either the staff knows that to be true personally, or this fact is noted on their account. (That note was written after the bank got extremely familiar with their cash management needs, for reasons.)

Very few customers routinely withdraw $50,000 in cash. We move to the next step on the flow chart. Here, the bank staff will begin to deploy some mix of truths, half-truths, and white lies.

One statement, which may be anywhere along that spectrum, is that the bank branch does not have $50,000 cash on hand. Across all bank branches in America, this is frequently actually, mathematically true. A true-ish variant of it is that the branch does actually have a bit more than $50,000 cash on hand. The branch needs it to service customers with routine cash needs, and the instant customer cannot be allowed to wipe out the bank’s on-hand cash reserves, because that will cause them to disappoint dozens or hundreds of customers between now and the rebalancing shipment of cash they will swiftly order. And then there is a false variant, where at some branches this is factually as operationally straightforward as exchanging a $20 bill for two rolls of quarters, but where the lie is institutionally excusable to save this customer from themselves.

Many people who have never withdrawn $50,000 in cash do not have great reasons for suddenly wanting to withdraw $50,000 in cash. It is quite likely they are being scammed or otherwise victimized. The bank, in consideration of its legal and ethical duties to its customer, would prefer to not facilitate this, even unknowingly. Over the universe of all people with this request, the bank knows, in its soul of corporate personhood, that it has actual knowledge of what is likely happening here.

And so, the staff will likely say that the bank has a rule, procedure, or request that the customer call them a day or two in advance of making large cash withdrawals. This will “allow us to get the cash together.” Now, in point of fact, there is a number that the branch manager could call to ask for an extraordinary shipment of physical currency, but this is mostly intended as a speedbump. Scams and other forms of exploitation rely on isolating the victim and pressuring them into making poor choices. Mandating a cooling-off period causes some scams to effervesce like dew in the morning sun.

Perhaps, as happens in many non-routine requests in banking, the customer will call in third-party professionals. Perhaps the customer, annoyed that the $50,000 they need to consummate a real estate transaction isn’t trivially on offer, might phone their real estate lawyer. This is music to the bank’s ears. Not every voice on a telephone is actually a lawyer, and not every member of the bar upholds its strict standards of professionalism and moral uprightness, but lawyers are so much easier to work with than civilians. And, should the matter be reviewed later, the bank will be able to document its reasonable reliance on representations made by a lawyer.

Fraudsters have frequently targeted real estate transactions in recent years. Banks are acutely aware of this; it’s covered extensively in their professional journals and in circulars from regulators. But banks, who have extensive experience with real estate deals, know that a few hiccups on closing are stressful for customers, but very rarely actually blow up transactions, certainly not like scams blow up bank customers.

The bank is unlikely to reach confidence, in this circumstance, in just a minute or two in the teller line. Many well-off people, with great relationships with their banks, with extensively paperworked transactions, will go through more than a half-hour of hoop jumping to get approval for anomalous transactions.

But suppose, for some reason, the calls do not happen and the extended due diligence is not performed. What is supposed to happen next? Well, typically at large money center banks (and here I cite both general industry knowledge and also sources familiar with banking procedure), the staff dealing directly with the customer will summon a second individual. Sometimes this is the branch manager, sometimes it is a peer. Sometimes the next action takes place verbally. Sometimes it happens in specifically built software which keeps an audit log of both staff signing off.

The bank invokes the Two Man Rule. (Yes, this has been renamed in many—but not all—formal documents recording procedural controls. Regulators have, generally, reviewed and approved those documents.)

If both individuals are satisfied that the anomalous transaction is not sufficiently hinky to refuse, it goes forward. This will generally require asking the customer about what they intend to do with $50,000 cash. Banks very rarely ask this question at $50 or $5,000.

Bankers, by law and custom, holistically review these situations. Elements considered include the account records, the experience of branch staff with this particular customer, and a host of context cues which the financial industry would prefer to dissimulate about.

If you are, for example, a lanky thirtysomething who waltzes into a branch in San Francisco and asks for a six figure wire to fund an investment, helpfully mentioning that you have the KYC/KYB information in a clear plastic folder, neither of the Two Men are likely to actually ask to read that folder. If you walk with a cane, if you speak with an accent, if you present as not really understanding the rituals you are engaged in, the bank and its staff will pay radically more attention to you, frequently not in ways you will enjoy.

Let us assume that a $50,000 withdrawal happens, through some pathway. It will have one more mechanical consequence. Very soon after the withdrawal, the bank will be obligated to file a Currency Transaction Report (CTR) with the Financial Crimes Enforcement Network (FinCEN), unless the customer has had a previously-approved status as someone who routinely needs to do this sort of thing, which almost no customers have. The CTR is a write-once read-probably-never document which mostly serves to get the customer’s banking information into a trivially searchable database for law enforcement.

And then what happens to the $50,000? Whatever the customer wants, really. If they want to put it in a shoebox and give it to a courier, it is, at that point, no longer the bank’s problem.

Style magazines sometimes publish hard-hitting journalism

In February 2024, the style publication The Cut published on its site, and concurrently in the print edition of New York Magazine, an article titled “The day I put $50,000 in a shoe box and handed it to a stranger I never thought I was the kind of person to fall for a scam.” It was written, in the first person, by a financial advice columnist who previously wrote for the New York Times business section.

The Cut and New York Magazine are owned by Vox Media, a private equity firm with material investments in advertising platforms (“We Create Premium Advertising Solutions”, “We Enable Media Companies To Build Modern Media Businesses”). Vox also publishes an eponymous website, notable for popularizing the term-of-art “explainer” and for publishing, about covid, analysis that aged more poorly than perhaps anything in the history of the written word. (It subsequently unpublished it.)

{kind=link}

Many of Vox’s publications are good at what they do. The shoebox piece successfully achieved virality and follow-on coverage by several media orgs. A media critic could point to reasons why, such as the specificity and viscerality, the it-could-happen-to-anyone framing, and the complicated mix of schadenfreude, voyeurism, and self-protective reassurance which make so-called “true crime” explorations so explosively popular.

Vox Media sell ads with rate cards justified by the storied legacy of New York Magazine, which has won Pulitzers before, against articles of the caliber produced by The Cut. The print edition of the piece is immediately preceded by a fashion spread for “TOM FORD Halter-neck Jumpsuit and Black Stamped Croc Bar Belt, at tomford.com” A similar item, U0269-FAX1105, on the site bears the price tag $5,790, which is capitalism’s surest signal as to who it thinks is reading a publication.

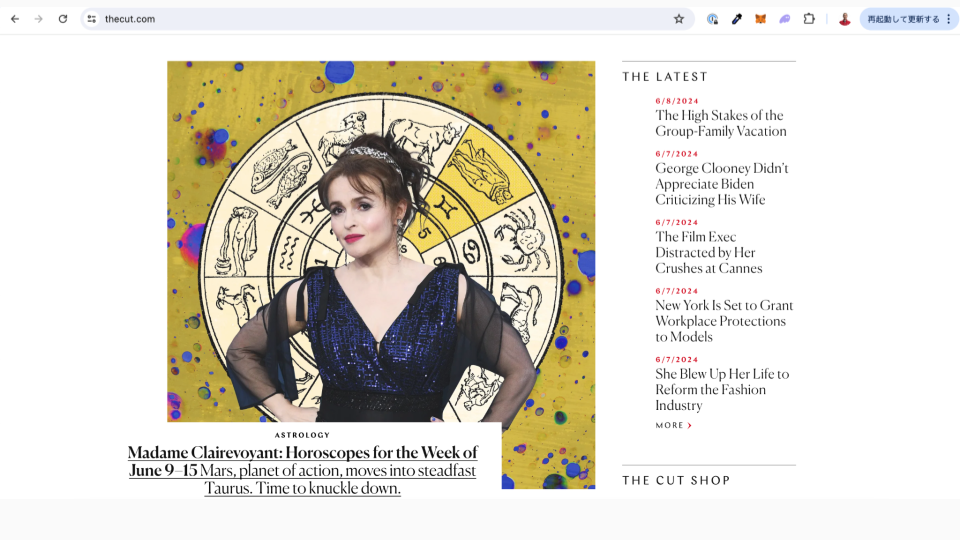

For a quick vibe check on editorial standards of any publication, by their fruits shall you know them: just read the headlines. I checked them the morning of a presentation on this investigation, and they were “The high stakes of the group family vacation”, “George Clooney didn’t appreciate Biden criticizing his wife”, “The film exec distracted by her crushes at Cannes”, and “Madam Clairevoyant: Horoscopes for the week of June 9-15. Mars, planet of action, moves into steadfast Taurus. Time to knuckle down.”

{kind=link}

Time to knuckle down… on hard-hitting journalism about banking procedures.

When I reached the bank, I told the guard I needed to make a large cash withdrawal and she sent me upstairs. Michael [a member of the scamming team] was on speakerphone in my pocket. I asked the teller for $50,000. The woman behind the thick glass window raised her eyebrows, disappeared into a back room, came back with a large metal box of $100 bills, and counted them out with a machine. Then she pushed the stacks of bills through the slot along with a sheet of paper warning me against scams. I thanked her and left.

As the piece went quite viral on Twitter, a number of people reached out to me. One specific question asked was “Are high-value withdrawal rooms a thing?”, which I answered, somewhat confusedly, “I could believe that there is, somewhere among 76,000 bank branches in the United States, a room designed to make $50,000 withdrawals. But no, the standard branch layout has no such room designed or designated.”

If a customer needs privacy, the branch has several rooms with doors, behind which banking business is routinely conducted. Those rooms are not fortresses. The branch is not a fortress. It's primarily a sales office for financial services that happens to handle some cash.

Then, I read the article, with a particular attention to the paragraph quoted above. I felt that several elements of this paragraph were inconsistent with the standard practice of banking.

I have an immense regard for journalism, generally, but the institution has been duped before. Stephen Glass comes to mind. One of the earliest bits of hard evidence against him was that he confabulated evocative details about the built reality of buildings he claimed to have visited. The shoebox piece contained much evocative detail, including some details I felt were, unbeknownst to almost all readers, likely to be checkable… and unlikely to have been checked.

Thus began an investigative journalism project, which ended up taking almost a year.

Reaching out to Vox Media

Having once worked for a Communications department, which very definitely does not endorse anything I say in this piece, I am aware of a social ritual of reporters and PR teams. You can send PR an email and ask them for a reply. By convention this is called a comment or a statement to pretend it is something vastly different in character than an excerpt from an email.

If one defects from this social ritual, many responsible professionals will conclude that one has something to hide. This is part of the reason why e.g. the largest banks in the world will swiftly answer questions asked by reporters working for, for example, a low-circulation weekly in Topeka, Kansas. This produces immense social utility, including by acting as an escalation pathway into the bank regarding, e.g., “Does the bank have a comment on why it is foreclosing on Ms. Mildred, who has shown this reporter a carefully maintained collection of checks that appear, to this reporter, to have been deposited?”

On February 22nd, 2024, I sent an email to Vox Media and asked for a comment. You don’t need to be bitten by a radioactive spider to do this. By custom, PR departments publish contact details widely, in part to avoid hostile journalists construing a lack of contact information as a refusal to comment.

There is, however, a performance of class that is helpful in getting PR departments to take you seriously. Mentioning that you are an avid Factorio player might not counsel an immediate reply to one’s questions. The following introduction is designed to compel one.

My name is Patrick McKenzie. I write a column titled Bits about Money, which frequently covers financial fraud and operational mechanics of banking infrastructure. I have previously appeared on Bloomberg and in the New York Times.

I read with interest the article about $50k in a shoebox, which was also published in the print edition of New York Magazine. I may reference it in future writing.

All claims in those paragraphs are true. Some people resent that one can assert authority simply because of implicit blessing of high-status institutions. I leave anyone to their aesthetic preferences, but will mention that this is a very important lesson for how halls of power in New York and Washington, D.C. work.

When the New York Times attempts to commission a piece from you, they will say apologetically that they can’t pay that well for it, but almost nobody writes for the Times for the money. You are paid in a different coin. Flash it, John Wick style, at a PR department, and it immediately takes you seriously, or it is quickly brought to task by New York’s hidden-in-plain-sight subculture of character assassins.

My email to the press contact asked a few questions and avoided explicitly broaching the question I was most curious about: Did the editorial process understand this piece to be an exercise in… creative writing? This felt unlikely, but magazines publish a spectrum of artifacts. Some pieces are roman à clefs, some are pastiches, some are based in a true story, and some are the more traditional understanding of journalism. On the text of it, the piece reads like it is reporting a true event, but it is in a style magazine and does run next to a piece titled Tweencore (“What the 13-and-under set is shopping for.”) and, you know, one may be forgiven some doubts.

A spokesperson for New York Magazine replied with a statement for publication which removed all doubt about how it perceived this story.

The story was thoroughly fact-checked prior to publication, and as part of this process, we reviewed the writer's bank withdrawal, recordings of phone calls and text messages with their scammer, and their statement to the police.

Since I had publicly expressed doubt that there was any fact checking process, I corrected the record.

Published statements or comments routinely occur in the context of a larger conversation. This is rarely mentioned, and I am promoting this subtext to text. There may have been any combination of on the record, on background, or off the record statements between myself and Vox Media. The world may never know.

But generally speaking, careful titration of how much information passes between PR and reporters, including restrictions (which are closer to handshake agreements than contracts) on what can be used where and when, enables a brisk favor-swapping economy. That economy has failed to function recently in the tech industry, as I discussed previously with Kelsey Piper. (Kelsey works in a different part of the Vocis machinae.)

When it does function, society gets the usual benefits of journalism, PR departments grumble a bit but play the game, the Bat Phone to mortgage servicing gets answered on the first ring, and advertisers sell their wares to willing customers to pay for it all.

Sources of doubt

So Vox Media’s statement through a spokesperson effectively definitively resolved my doubts about editorial processes… but this did not resolve my doubts about banking procedure.

Fraud investigators, law enforcement, and journalists alike frequently start with intuition then backfill with objective facts. My intuitions were screaming.

The article does not actually name the bank or the bank branch, despite a scene unambiguously set within it, despite the centrality of its failure to the narrative, despite repeated identification of firms that were utterly uninvolved. The transaction does not proceed as what a bank expects to happen if someone asks for the entirety of their savings account in cash. Physical details provided for flavor purposes are very rare in the universe you live in.

The claimed fact checking process struck me as… other than robust, in worlds where parts of the article were not factually accurate.

For example, there are many ways to “review a bank withdrawal.” That review can involve five or more parties, and I’ve been on almost all ends of it at various times. Some “reviews” are low-friction but low-robustness, such as e.g. asking someone to see a screenshot of their mobile phone or a printout of a bank statement.

As I once told a colleague in an unrelated context: a printed bank statement is of limited probative value because it could be forged by a bright high school student.

The financial industry has a variety of ways to resolve this, depending on how much time and toil it wants to expend on the investigation. For example, you can call the financial institution which issued the statement in question, announce that you are in a room with their customer, and then ask their customer to ask them to read the financial institution’s copy of the statement into the open line. Many people I have told about this ritual assume that, due to security concerns, no bank will engage in it. Nope! This is extremely routine and will happen tens of thousands of times next Tuesday. It is obviously more trustworthy than a copy of the statement whose chain of custody includes a non-bank actor.

Anyhow, some years after cracking wise about bright high school students, I chanced upon an infelicity which happened to New York Magazine. It published that a Stuyvesant high school student had made $72 million trading stocks and was shortly to open a hedge fund.

This is obvious nonsense and would be detected within seconds of conversation by anyone professionally involved in hedge funds, but we have a ritual in our society which blesses some writers as being owed the benefit of the doubt when they publish obvious nonsense. If it ran in the pages of New York Magazine, and New York Magazine engaged its standard fact checking process by sending someone to Stuyvesant to review a bank statement, and that piece of paper said Chase at the top and an eight figure number at the bottom, then the clearly the story is defensible, right.

No! Of course not! New York Magazine got punked by a teenager.

And so, reading New York Magazine’s newest written statement about thoroughly fact checking a bank withdrawal, I thought “After ten years memories fade. Vox is currently wearing New York Magazine as a skin-suit, so who knows if anyone involved in that fracas is still around. Perhaps current staff reviewed the newest issue’s most important transaction in an other-than-robust fashion.”

Texts from the scammer? Voice recordings? A statement to the police? All of these struck me as highly correlated rather than being independent evidence: all reliable if one trusts the writer, and all unreliable if one does not trust the writer.

Never having employed or encountered this writer myself, before she wrote things I believed to be improbable about banking procedure, I reflected on what I do trust.

I trust the physical reality of the world. I trust that it is very difficult to corrupt the archives of societal institutions.

The physical reality of bank branches

Vanishingly few bank branches put teller windows on the second floor. Many people have not ever had reason to deeply consider this true fact about the world. Relatively few people have ever made real estate decisions about siting bank branches or sketched layouts for them.

By coincidence, my father has. And, as someone who listened attentively at the dinner table and on car rides as he geeked out with his eldest son about the relative merits of various corners in Chicago, when I read that there was a bank branch in New York City with thick glass on the second floor, I thought “If that unicorn exists, I can probably narrow it down to a single physical location.”

New York City, ye capital of the world, ye center of global finance, ye city which never sleeps: poets say you contain stories beyond numbering, but bike messengers can count your bank branches. A few hundred. Done. A diligent person could walk into every last one. (Of course the public can just walk into bank branches. That is what they are for.)

I started by attempting to narrow the set, to save some shoe leather. One gets a free 90%+ reduction by narrowing it to one bank in particular. Bank regulators keenly track deposit share concentration (and, therefore, bank branch concentration) in major markets, and NYC, the majorest market, is gardened with an exactitude that makes the feng shui look effortless.

Who knows the bank? Well, Vox (by implication of their statement) must know the bank, and the writer certainly knows the bank, and perhaps one of these would give an on the record comment naming the bank.

The writer engages in freelance journalism, has a professional website which lists her email address, and swiftly answered a question from another writer, on the record.

Bank of America.

Now we are getting somewhere.

Bank of America will trivially give you a list of all Bank of America locations in Brooklyn, for many reasons, including “We would certainly hope you find our financial centers for your financial services needs. We didn’t build this branch footprint and lease out desirable locations for a half century and sweat the details about curb cuts for the sheer joy of it all.”

One can, if one is unusually punctilious, cross reference their list against public records.

One useful sort of public record is the Office of the Comptroller of the Currency’s weekly bulletin, which includes all bank branch closings for nationally chartered institutions in the United States. Why would one care about those bulletins? An investigation, conducted in February 2024, about branches open on October 31st, 2023, might otherwise miss some which closed in the interim. And so I told my research assistant to read a few months of bulletins. (He surprised me by saying there is a search engine these days. Well, this wire transfer compliance influencer learned a new trick in 2024.)

And so we had twenty two Bank of America branches in Brooklyn to look at.

I’m in Chicago, and flying to Brooklyn to spend three days walking into branches seems like an obviously irrational use of my time. So, in the finest tradition of publications assigning scutwork to junior employees, I sent Sammy to Brooklyn instead.

We excluded any buildings which physically didn’t have a second floor. We used sophisticated techniques taught in journalism school, like the fact you can press ten buttons on an iPhone and then someone at a bank in Brooklyn will immediately answer questions like “Does your branch have a second floor?”

We kept a detailed spreadsheet, in the expectation we might eventually have to show New York media outlets that we had done our homework. A timestamped call here, a Street View there, our search area narrowed precipitously.

The final round of investigation involved Sammy physically entering bank branches, walking to the second floor, and looking for physical details consistent with the story as published.

This is a long way to say: I am very confident indeed that the only place in the world the described bank transaction could possibly have taken place at is 1 Flatbush Avenue, at the teller window, on the second floor. Right here.

We took this photo in March 2024, only weeks after publication of the original article.

And then we entered a long, long holding pattern, trying to find one trusted institution to say that, as of earlier than February 2024, they understood the transaction to either a) definitely have taken place at 1 Flatbush Avenue or b) definitely not have taken place at 1 Flatbush Avenue.

In which we became acquainted with brisk walks across Brooklyn

If the incident took place in the physical world, then the geospatial reality of the world imposes some constraints on the narrative. The writer unambiguously locates their narrative in Brooklyn. But Brooklyn is large.

Could we narrow it down? Could we do that using only independent, trustworthy information?

I trust, for example, that the city of New York keeps mostly accurate records about who owns property. These are quite useful for e.g. facilitating the orderly operation of the country's largest real estate market. The records are publicly available through the Automated City Register Information System (ACRIS).

I learned two things from ACRIS in early 2024.

One was an address on a mortgage. That address is, factually, a thoroughly doable walk from 1 Flatbush Avenue.

The other: this outsider, trusting at face value representations made by a news publication about the socioeconomic status of the subject of a story, did not successfully predict other facts present on that mortgage.

Socioeconomic class, unfortunately, has a great deal of bearing on how a bank would choose to interact with an individual. This is particularly true as one approaches either end of the socioeconomic spectrum, away from the mass market that most people assume banks must be serving at all times. We have often discussed discontinuities in service at the lower end of the spectrum in Bits about Money. There exist… other discontinuities.

I realize that commenting on the socioeconomic status of a crime victim is uncouth, particularly in ways they might not choose to describe themselves. Class is unfortunately essential to understanding what actually happened at 1 Flatbush Avenue on October 31st, 2023. Permit me a brief recital of the source of my confusion.

This outsider perceived a through-line of the Cut piece as being that the writer made other-than-rational decisions about $50,000 because their financial life was on the line. Here are some select non-consecutive paragraphs reproduced verbatim, with bolding added to highlight statements this outsider apparently read incorrectly.

Calvin [a member of the scamming team] wanted to know how much money I currently had in my bank accounts. I told him that I had two — checking and savings — with a combined balance of a little over $80,000. As a freelancer in a volatile industry, I keep a sizable emergency fund, and I also set aside cash to pay my taxes at the end of the year, since they aren’t withheld from my paychecks.

I almost laughed. I told him I was quite sure that my husband, who works for an affordable- housing nonprofit and makes meticulous spreadsheets for our child-care expenses, was not a secret drug smuggler. “I believe you, but even so, your communications are probably under surveillance,” Calvin said. “You cannot talk to him about this.” I quickly deleted the text messages I had sent my husband a few minutes earlier. “These are sophisticated criminals with a lot of money at stake,” he continued. “You should assume you are in danger and being watched. You cannot take any chances.”

Fifty thousand dollars is a lot of money. It took me years to save, stashing away a few thousand every time I got paid for a big project. Part of it was money I had received from my grandfather, an inheritance he took great pains to set up for his grandchildren before his death. Sometimes I imagine how I would have spent it if I had to get rid of it in a day. I could have paid for over a year’s worth of child care up front. I could have put it toward the master’s degree I’ve always wanted. I could have housed multiple families for months. Perhaps, inadvertently, I am; I occasionally wonder what the scammers did with it.

Because I had set it aside for emergencies and taxes, it was money I tried to pretend I didn’t have — it wasn’t for spending. Initially, I was afraid that I wouldn’t be able to afford my taxes this year, but then my accountant told me I could write off losses due to theft. So from a financial standpoint, I’ll survive, as long as I don’t have another emergency — a real one — anytime soon.

These statements, and others throughout the article, conjured a particular image for me. It was that the writer was upper middle class, dealt with a bit of financial anxiety common to many individuals in precarious or not-particularly-remunerative employment circumstances, and was abused by professional con artists in a calculated fashion to prey upon this financial insecurity.

When recounted these same statements, my friend Byrne Hobart, who has actually lived among this social milieu before, laughed knowingly and said “Ah, family money.”

I will now add three true statements to the above sketch, in the hopes that you understand this transaction the way that a Bank of America teller understood it.

The writer’s positive home equity, trivially available to the bank which wrote their mortgage, is well in excess of ten years of the median household income for New York City. The writer is the president of the family charitable foundation, which per its annual filings with the IRS has in the recent past held approximately $2 million in marketable securities. And the family estate in Connecticut (which the writer’s parents live at) was featured in the local paper, highlighting two hundred years of history.

Discovering these facts radically changed my impression of why, per the writer’s written communication with me, she was not asked for the purpose of a $50,000 withdrawal by any bank staff. It no longer looks like a surprising lapse in procedure, when someone attempted to empty their entire savings account and wasn’t even half-heartedly counseled about caution. It looks like trivial cash management of a well-off, presumptively sophisticated client, whose household, resources, and probable financial future were thoroughly known to the bank.

Would the bank prefer the teller to ask one more question in this circumstance? Perhaps. But it won’t lose sleep over the matter.

Bank of America was asked about this transaction by the New York Times: “‘We have extensive efforts to warn clients about avoiding scams,’ said a Bank of America spokesman, William P. Halldin, via email. The bank declined to comment further.” (The Times, citing policy, refused to confirm the bank branch it understood the transaction to have taken place at.)

And thus we return to our earlier question: can we find an institution which will divulge where this transaction was claimed to have taken place at? Vox Media, the writer, and the New York Times have all been asked, and we do not have an answer yet.

Enter the Financial Crimes Enforcement Network

Bank of America is one of the largest depository institutions in the world, and reliably files Currency Transaction Reports when someone moves $10,000 or more into, or out of, the bank in cash. I thought it would be extremely unlikely that FinCEN would cough one of these up to anyone who asked.

But a recent development in Freedom of Information Act jurisprudence gave me some hope: the FOIA now, per the Ninth Circuit, allows for “statistical aggregate data” to be FOIAed. And I thought there was some hope that FinCEN would, rather than showing me a very private Currency Transaction Report, answer a simple question about statistical aggregates.

So I filed a FOIA request, 2025-FINF-00126, asking for a statistical calculation to be done:

How many currency transaction reports were filed. In Brooklyn. For a withdrawal of between $48,000 and $52,000. On October 31st, 2023. Broken down by branch address.

FinCEN efficiently processed this FOIA request, returning a definitive answer in less than two weeks: hell no. It asserted the same argument rejected by the 9th Circuit, that responding would require creating a new record (the results of the SQL query) and therefore it had no obligation to do so. It also asserted a statutory exemption which very broadly applied to many records kept by FinCEN. On reading the statutes, I thought FinCEN likely had the right of them, even if it was unlikely to prevail on the statistical aggregate issue.

Drats. It was worth a shot.

New York’s Finest foil FOIL for a time

The statement from Vox Media claimed that the writer had filed a police report.

From the perspective of a fact-checker, police reports serve a useful tripwire function. Lying on one is a crime. It is not a particularly serious crime (a class A misdemeanor, which also covers “spilling a drink on someone” and “shoplifting a bottle of Tide”).

One is welcome to one’s guess as to how often New York prosecutors enforce this law, particularly against people in our social class. But it is a useful Schelling point for society: a news publication can gesture in the direction of a police report, and say “Well, everyone knows what a police report means”, and we all pretend that it means a police report necessarily contains no lies.

No police officer need disabuse journalists of their illusions here. Should a publication ever get put to the question, it will immediately pivot into “We didn’t say we agreed with or believed anything on the police report. We simply neutrally reported the demonstrable fact of the police report. Obviously we intended nothing else by bringing up a police report.”

But police reports remain useful even in a world where they sometimes contain lies, because they establish paper trails which are extremely difficult to retrospectively fudge.

I was most interested in two facts on the police report.

One was metadata: when was this report received? (It obviously reads a bit differently if the report was created in response to the fact-checker asking for it, right.) The other: did, prior to the publication of the story, the writer consistently cite 1 Flatbush Avenue, the only location in the physical universe the transaction could have taken place at, as the location the transaction took place at?

I tried to get that police report, by several methods. By June 2024, getting impatient, I was at the point of forcing enthusiastically encouraging the NYPD to follow the law and provide it to me.

Police reports, like many public records, are retrievable under the Freedom of Information Law, New York state’s legislation which mirrors the federal FOIA. The statutory deadlines are five business days to acknowledge a request, and then twenty business days (or such time reasonably required) to release the records or cite an exemption under the law for not disclosing them.

I filed FOIL-2024-056-16750 on June 26th, 2024. On the last possible day, the NYPD updated its timeline to successfully locate a police report: it would need until November. OK, fair enough. I was a bit busy myself, being involved in a house purchase and move, and my one paper copy of a style magazine was hanging out in a box in the basement while we repainted. Perhaps the New York Police Department, annual budget $5.8 billion, was likewise quite busy.

November came. November went.

Eventually, concerned that Santa would not deliver the Christmas present I most wanted, I began to press the NYPD for answers. I did this using a voice and mien which I call Dangerous Professional. Three messages, one phone call, no dice.

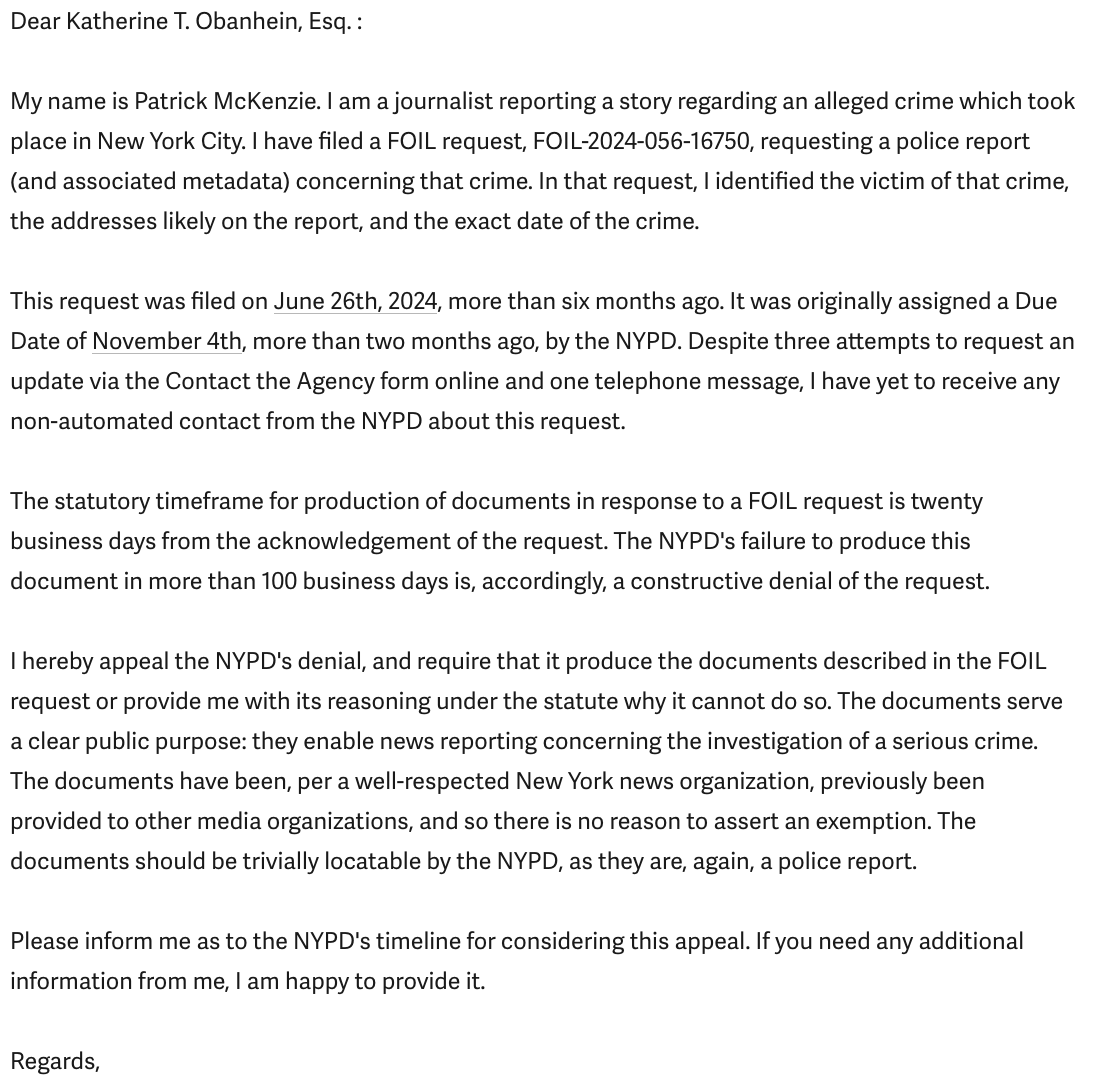

And so, in February 2025, after a full six months of waiting on the NYPD, I got out my call log and penned a FOIL appeal. After a brief recitation of the procedural history, that letter did a bit of calculated knife twisting:

{kind=link}

This request was filed on June 26th, 2024, more than six months ago. It was originally assigned a Due Date of November 4th, more than two months ago, by the NYPD. Despite three attempts to request an update via the Contact the Agency form online and one telephone message, I have yet to receive any non-automated contact from the NYPD about this request.

The statutory timeframe for production of documents in response to a FOIL request is twenty business days from the acknowledgement of the request. The NYPD's failure to produce this document in more than 100 business days is, accordingly, a constructive denial of the request.

I hereby appeal the NYPD's denial, and require that it produce the documents described in the FOIL request or provide me with its reasoning under the statute why it cannot do so.

An attorney for the NYPD wrote back, forecasting a response within the statutory timeframe (10 business days for an appeal). The substantive response said that the appeal was moot because… the Records Access Officer had, subsequent to my appeal, made a determination that the NYPD did indeed keep police reports and could indeed release them in response to FOIL requests.

Oh happy day.

The police report contains a statement recorded by the police made on October 31st, 2023. I have lightly rewritten police shorthand and corrected some inconsequential spelling mistakes:

Complainant/victim further states listed perpetrator stated complainant/victim needed to pay in order to avoid being arrested. Complainant/victim states she withdrew $50,000 in U.S. currency from Bank of America, located at 1 Flatbush Avenue, at 3:10 PM.

And there we have it: reliable chain of custody to a claim made about the physical world at a known time, within hours of the alleged incident. This transaction was alleged to have happened at 1 Flatbush Avenue. Months later, in writing of her memories of the day, the writer offered a seemingly inconsequential detail about going up stairs to visit a teller window.

That seemingly inconsequential detail is, if one has a very particular set of interests, and is willing to put an irrational amount of work in, independently verifiable. Of all the bank branches in all the towns in all the world, the only one where a Bank of America teller awaits Brooklyn socialites behind thick glass on the second floor is, indeed, 1 Flatbush Avenue.

This would be a very different piece if that police report, or any other documentation at a trusted institution, named e.g. 266 Broadway instead.

As for the rest of the shoebox piece? I have no informed point of view on anything in a style magazine, except for the banking.

Want more essays in your inbox?

I write about the intersection of tech and finance, approximately biweekly. It's free.